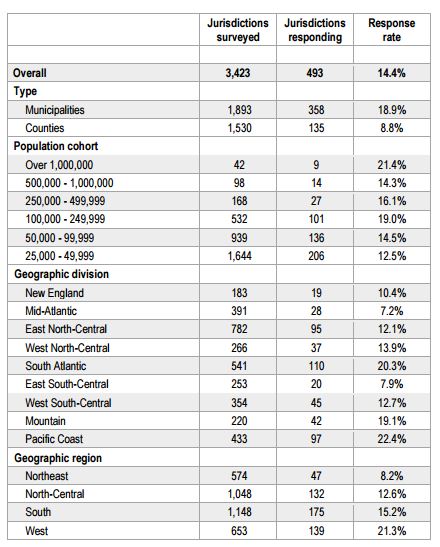

Nearly 500 U.S. cities and counties with populations over 25,000 participated in a recent survey by the International City/County Management Association (ICMA) and the Smart Cities Council on a range of topics around smart city initiatives, policies and procurement practices. There were definitely some surprises in the results – and some findings that public sector leaders most everywhere will find familiar.

Survey highlights were presented during last month's Smart Cities Week event in Washington, D.C. by Council Chief Scientist Stuart Cowan and Jelani Newton, Director of Survey Research with ICMA.

Some of the key findings include:

- Nearly half (49%) of survey respondents identified smart city technologies as a top priority in the public safety sector

- Smart payments and finance was the technology area in which responding communities are most active, with 60% of respondents identifying initiatives in this area as actively deployed

- Also included in the top five technology areas with initiatives in active deployment were customer service/public engagement (40%), energy (39%), water and wastewater (38%) and telecommunications (36%)

Cowan noted the discrepancies in sectors that cities and counties are actively implementing smart technologies in. For example, 59% are doing projects in smart payments and finance yet only 5% are active in smart technology in food and agriculture.

Benefits and barriers

The five benefits most frequently identified by responding communities as being very important in motivating their governments to implement or expand smart city initiatives included:

- Economic development 44%

- Capital and/or operational cost savings 43%

- Resiliency for critical operations 43%

- Enhanced services for residents 38%

- Safety and security benefits (37%).

Not surprisingly, when asked about barriers to implementing smart technologies, 42% of respondents identified budget limitations. They also cited the need for more internal capacity (21%) and the need for more supporting infrastructure (15%) as other important barriers.

Not surprisingly, when asked about barriers to implementing smart technologies, 42% of respondents identified budget limitations. They also cited the need for more internal capacity (21%) and the need for more supporting infrastructure (15%) as other important barriers.

Newton pointed out that size of a community tends to influence its involvement in smart cities activities, with smaller communities less active due to capacity challenges.

Cowan noted several results that were unexpected, including that only 27% of respondents are working with other cities and counties to aggregate demand and increase their purchasing power in procurement of smart technologies.

He also expressed surprise that planners are not more actively involved in smart city projects and suggested the number of respondents engaged in public-private partnerships was higher than expected.

Download a full summary of ICMA/SCC survey results here.

You may also be interested in…

Smart Cities Readiness Guide

Smart Cities Solutions

Policy Brief: Smart Infrastructure Unlocks Equity and Prosperity for Our Cities and Towns